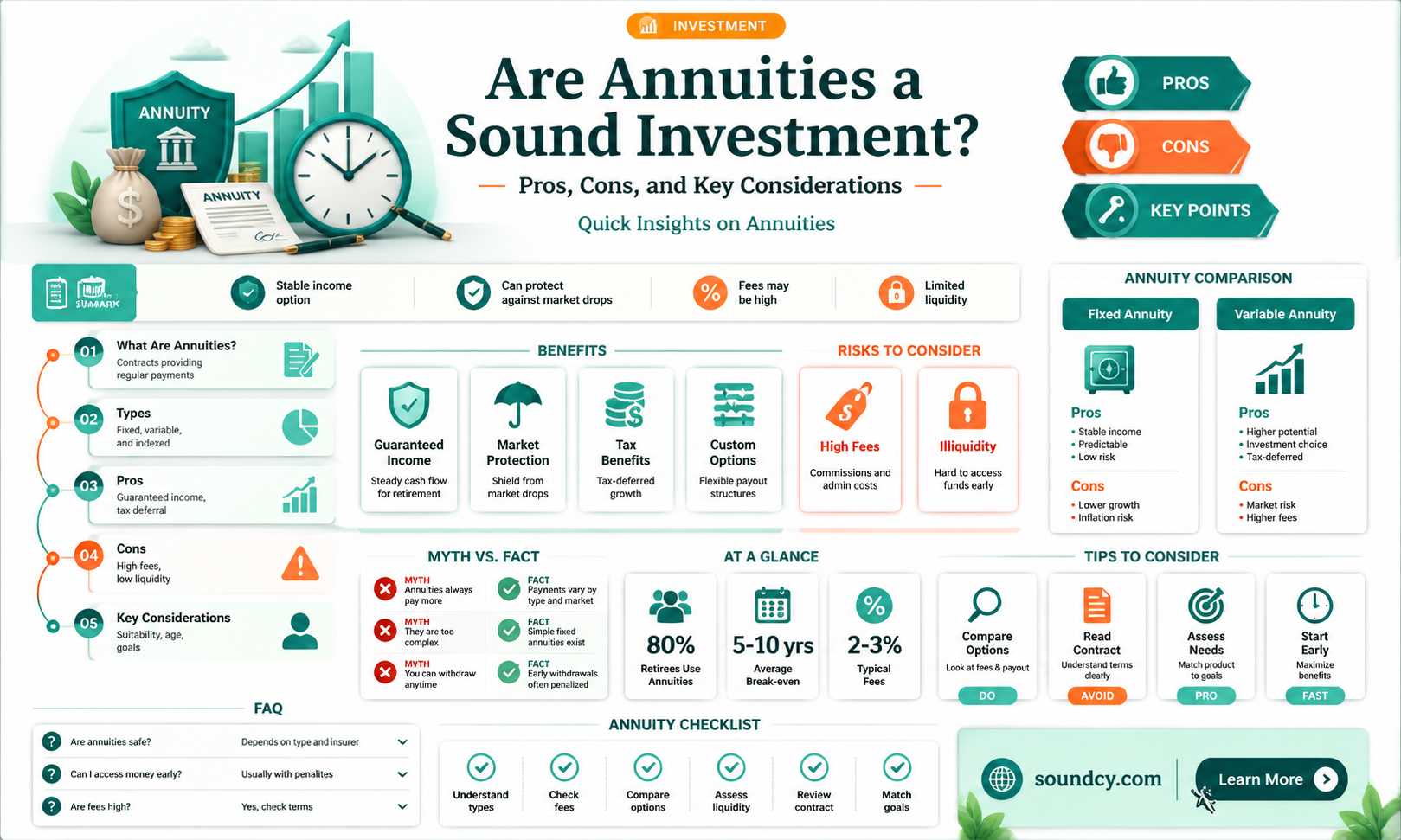

Annuities have long been touted as a reliable financial tool for retirement planning, offering a steady stream of income in exchange for an initial lump sum or periodic payments. However, whether they are a sound investment depends on individual financial goals, risk tolerance, and market conditions. Proponents argue that annuities provide guaranteed income, tax-deferred growth, and protection against outliving savings, making them particularly appealing for retirees seeking stability. Critics, however, highlight high fees, limited liquidity, and potentially lower returns compared to other investment options. Ultimately, the suitability of annuities as an investment hinges on careful consideration of one’s unique financial situation and long-term objectives.

Explore related products

What You'll Learn

- Annuity Pros and Cons: Weighing benefits like guaranteed income against drawbacks such as fees and inflexibility

- Types of Annuities: Fixed, variable, indexed—understanding differences to match financial goals and risk tolerance

- Tax Implications: Exploring tax-deferred growth and potential tax burdens on annuity distributions

- Fees and Hidden Costs: Analyzing surrender charges, management fees, and their impact on returns

- Alternatives to Annuities: Comparing annuities with other retirement tools like IRAs, 401(k)s, or stocks

![]()

Annuity Pros and Cons: Weighing benefits like guaranteed income against drawbacks such as fees and inflexibility

Annuities can be a complex financial product, and determining whether they are a sound investment depends heavily on an individual's financial goals, risk tolerance, and retirement planning needs. One of the most significant pros of annuities is the guaranteed income they provide. In an era where traditional pension plans are becoming rare, annuities offer a steady stream of payments, often for life, which can be particularly appealing for retirees seeking predictable cash flow. This feature can help mitigate the risk of outliving one's savings, a common concern among retirees. Additionally, certain types of annuities, such as fixed annuities, provide a guaranteed rate of return, offering stability in volatile markets.

Another advantage of annuities is their tax-deferred growth. Like other retirement accounts, such as 401(k)s and IRAs, annuities allow investments to grow without being taxed until withdrawals are made. This can be beneficial for long-term savings strategies, as it allows for compounding growth over time. Furthermore, annuities can serve as a hedge against market volatility. Variable annuities, for instance, offer investment options similar to mutual funds but often include riders that guarantee a minimum income or protect against downside risk, providing a safety net during market downturns.

Despite these benefits, annuities also come with notable drawbacks. One of the most significant cons of annuities is their high fees. Annuities often involve multiple layers of fees, including surrender charges, administrative fees, and investment management fees. These costs can erode returns over time, making annuities less attractive compared to lower-cost investment options like index funds. Additionally, annuities are often criticized for their inflexibility. Once funds are committed to an annuity, accessing the principal can be difficult and costly, as early withdrawals typically incur steep penalties.

Another drawback is the complexity of annuity products. With various types of annuities—fixed, variable, indexed, and immediate—understanding the nuances of each can be challenging. Misunderstanding the terms or choosing the wrong type of annuity can lead to unfavorable outcomes. Moreover, annuities may not keep pace with inflation, particularly in the case of fixed annuities with low interest rates. This can diminish the purchasing power of the guaranteed income over time, especially in high-inflation environments.

Finally, the opportunity cost of investing in annuities must be considered. By locking funds into an annuity, individuals may miss out on potentially higher returns from other investments, such as stocks or real estate. This trade-off between guaranteed income and growth potential is a critical factor in deciding whether annuities align with one's financial objectives. In conclusion, while annuities offer valuable benefits like guaranteed income and tax-deferred growth, their drawbacks—including high fees, inflexibility, and complexity—make them a less suitable option for some investors. Careful consideration of one's financial situation and long-term goals is essential before committing to an annuity.

Crafting Compelling Narratives: Mastering the Art of Writing Sound Stories

You may want to see also

Explore related products

![]()

Types of Annuities: Fixed, variable, indexed—understanding differences to match financial goals and risk tolerance

When considering whether annuities are a sound investment, it's essential to understand the different types available and how they align with your financial goals and risk tolerance. Annuities are financial products designed to provide a steady income stream, typically during retirement, but they come in various forms, each with distinct features and benefits. The three primary types of annuities are fixed, variable, and indexed, and grasping their differences is crucial for making an informed decision.

Fixed Annuities are often considered the most conservative option among the three. With a fixed annuity, the insurance company guarantees a specific interest rate on your investment for a certain period, typically ranging from one to ten years. This predictability makes fixed annuities appealing to risk-averse investors who prioritize stability and guaranteed income. They are particularly suitable for individuals nearing retirement or those seeking to preserve capital while generating a steady, reliable income stream. However, the trade-off is that fixed annuities generally offer lower returns compared to other types, especially in a rising interest rate environment.

Variable Annuities, on the other hand, are better suited for investors with a higher risk tolerance and a longer investment horizon. Unlike fixed annuities, the returns on variable annuities are tied to the performance of underlying investment portfolios, often consisting of mutual funds. This means that the income payments and the value of the annuity can fluctuate based on market conditions. While this exposes the investor to market risk, it also offers the potential for higher returns, making variable annuities an attractive option for those willing to accept volatility in exchange for growth opportunities. These annuities are ideal for individuals who have a longer time frame before retirement and want their investments to have the potential to outpace inflation.

Indexed Annuities strike a balance between the stability of fixed annuities and the growth potential of variable annuities. These annuities earn interest based on the performance of a specific stock market index, such as the S&P 500, but with some level of protection against market downturns. Indexed annuities typically offer a minimum guaranteed interest rate, ensuring that even if the index performs poorly, the annuity’s value won’t decrease. Additionally, they often include a cap or participation rate, which limits the upside potential but provides a measure of security. This hybrid nature makes indexed annuities suitable for moderate-risk investors who want some exposure to market gains without the full risk of variable annuities.

Understanding the differences between fixed, variable, and indexed annuities is key to aligning your investment choice with your financial objectives and risk tolerance. Fixed annuities are ideal for those seeking guaranteed income and capital preservation, while variable annuities cater to investors willing to take on more risk for potential higher returns. Indexed annuities offer a middle ground, providing some market exposure with downside protection. By carefully evaluating these options, you can determine which type of annuity best fits your retirement planning needs and helps you achieve your long-term financial goals.

Ultimately, whether annuities are a sound investment depends on your individual circumstances, including your age, financial situation, and retirement goals. Each type of annuity serves a different purpose, and their suitability varies based on your risk tolerance and desired outcomes. Consulting with a financial advisor can provide personalized guidance to ensure that the annuity you choose aligns with your overall investment strategy and helps secure your financial future.

Unveiling the Tuba's Magic: How Air and Brass Create Deep Sounds

You may want to see also

Explore related products

![]()

Tax Implications: Exploring tax-deferred growth and potential tax burdens on annuity distributions

Annuities can offer tax-deferred growth, which is one of their most appealing features as an investment vehicle. This means that the earnings within the annuity—such as interest, dividends, or capital gains—are not taxed until they are withdrawn. This tax deferral allows the investment to grow at a compounded rate, potentially faster than a taxable account where annual gains are subject to taxation. For individuals in higher tax brackets, this can be particularly advantageous, as it allows them to postpone taxes until retirement when they may be in a lower tax bracket, thus reducing their overall tax liability.

However, the tax-deferred nature of annuities comes with a trade-off: distributions from annuities are generally taxed as ordinary income. When you begin taking withdrawals, whether as a lump sum or as regular payments, the earnings portion of the distribution is taxed at your ordinary income tax rate. This is in contrast to other investment vehicles, such as Roth IRAs, where qualified distributions are tax-free. For those who expect to be in a similar or higher tax bracket during retirement, this could result in a significant tax burden, potentially offsetting some of the benefits of tax-deferred growth.

Another important consideration is the impact of required minimum distributions (RMDs) on annuities held in tax-deferred accounts, such as traditional IRAs or 401(k)s. Once you reach a certain age (currently 73 for most retirees), the IRS mandates that you begin taking RMDs from these accounts. These distributions are taxed as ordinary income, and failing to take them can result in substantial penalties. For annuities within these accounts, RMDs can complicate the distribution strategy, especially if the annuity is designed to provide a guaranteed income stream, as the RMDs may force larger withdrawals than planned, increasing the tax burden.

Non-qualified annuities, which are purchased with after-tax dollars, have different tax implications. When distributions are taken, only the earnings portion is taxed as ordinary income, while the principal (the amount originally invested) is returned tax-free. This can provide more flexibility in managing tax liabilities, as you can control the timing and amount of withdrawals to some extent. However, if the annuity is annuitized (converted into a stream of payments), the taxation becomes more complex, as each payment is divided into a return of principal and taxable earnings based on an exclusion ratio determined by the IRS.

Finally, it’s crucial to consider the potential for future tax law changes when evaluating the tax implications of annuities. While current tax rates and laws provide a framework for planning, there is always the possibility of legislative changes that could affect how annuities are taxed. For example, if tax rates increase in the future, the tax burden on annuity distributions could become more significant. Therefore, investors should weigh the current benefits of tax-deferred growth against the uncertainty of future tax environments and their potential impact on retirement income.

In conclusion, while the tax-deferred growth of annuities can be a powerful tool for building wealth, the potential tax burdens on distributions must be carefully considered. Understanding how annuities are taxed, both in terms of earnings and distributions, is essential for determining whether they are a sound investment within the context of an individual’s overall financial and tax planning strategy. Consulting with a tax professional can provide personalized insights to maximize the benefits and minimize the drawbacks of annuities.

How to Send Audio Files Efficiently Using Ubuntu: A Quick Guide

You may want to see also

Explore related products

![]()

Fees and Hidden Costs: Analyzing surrender charges, management fees, and their impact on returns

When evaluating whether annuities are a sound investment, one of the most critical aspects to consider is the fees and hidden costs associated with these financial products. Annuities often come with a complex fee structure that can significantly erode returns over time. Among the most prominent fees are surrender charges, which are penalties imposed if you withdraw funds from the annuity before a specified period, often ranging from 5 to 10 years. These charges can be as high as 10% or more of the withdrawal amount in the early years, making it costly to access your own money. For investors who may need liquidity or flexibility, surrender charges can be a substantial drawback, as they effectively lock in your funds and reduce the annuity's overall value if you need to make early withdrawals.

In addition to surrender charges, management fees are another significant cost factor in annuities. These fees cover the administrative and investment management expenses associated with the annuity contract. Variable annuities, in particular, often carry higher management fees because they involve professionally managed investment portfolios. While these fees may seem small on a percentage basis (typically 1-3% annually), they compound over time and can substantially reduce the growth of your investment. For example, an annuity with a 2% annual management fee could result in tens of thousands of dollars in lost returns over a 20- or 30-year period, compared to lower-cost investment alternatives like index funds.

Another hidden cost to watch for is the mortality and expense (M&E) fee, which is common in variable annuities. This fee, usually around 1-1.5% annually, covers the insurance company's risk and operational costs. While it may seem minor, it adds to the overall expense ratio, further diminishing returns. Additionally, some annuities include rider fees for optional benefits like guaranteed lifetime income or long-term care coverage. While these riders can provide valuable protections, they come at a cost that must be weighed against the potential benefits.

The cumulative impact of these fees on returns cannot be overstated. Studies have shown that the long-term returns of annuities often lag behind those of lower-cost investment vehicles due to their fee structure. For instance, a hypothetical investment of $100,000 in a variable annuity with a 3% annual fee could result in a significantly lower balance after 20 years compared to the same investment in a low-cost mutual fund or ETF with a 0.5% fee. This disparity highlights the importance of carefully analyzing fees when considering annuities as part of your investment strategy.

To make an informed decision, investors should scrutinize the fee schedule of any annuity contract and compare it to alternative investment options. Tools like fee calculators can help quantify the long-term impact of these costs on your returns. Additionally, working with a fee-only financial advisor can provide objective guidance, as they are not incentivized to sell high-fee products. Ultimately, while annuities can offer benefits like guaranteed income and tax deferral, their fees and hidden costs must be carefully weighed to determine if they align with your financial goals and risk tolerance.

Soundproofing Secrets: How NYC Apartments Block Out City Noise

You may want to see also

Explore related products

$14.99

![]()

Alternatives to Annuities: Comparing annuities with other retirement tools like IRAs, 401(k)s, or stocks

When considering whether annuities are a sound investment, it’s essential to compare them with other retirement tools like IRAs, 401(k)s, and stocks. Each of these options serves different financial goals, risk tolerances, and retirement timelines. Annuities offer guaranteed income streams in retirement, which can be appealing for those seeking stability. However, they often come with high fees, limited liquidity, and lower growth potential compared to other investments. In contrast, IRAs (Individual Retirement Accounts) and 401(k)s provide tax advantages and greater flexibility in investment choices, allowing for potentially higher returns over time. These accounts are ideal for individuals willing to manage their investments actively or rely on professional advisors.

Stocks are another alternative to annuities, offering the potential for significant growth but with higher volatility and risk. Unlike annuities, which provide predictable income, stocks require a long-term investment horizon and the ability to withstand market fluctuations. For retirees or those nearing retirement, the risk associated with stocks may outweigh the potential rewards, making them less suitable as a primary retirement tool. However, for younger investors with decades until retirement, stocks can be a powerful way to build wealth through compounding returns.

IRAs and 401(k)s stand out as strong alternatives to annuities due to their tax benefits and diversification opportunities. Traditional IRAs and 401(k)s allow contributions to grow tax-deferred, while Roth versions offer tax-free withdrawals in retirement. These accounts can hold a mix of stocks, bonds, mutual funds, and ETFs, enabling investors to tailor their portfolios to their risk tolerance and goals. Unlike annuities, which lock in funds for a specified period, IRAs and 401(k)s generally offer more liquidity, though early withdrawals may incur penalties.

For those seeking income stability without the complexities of annuities, bond investments or dividend-paying stocks can be viable alternatives. Bonds provide regular interest payments and are less volatile than stocks, though their returns are typically lower. Dividend-paying stocks offer periodic cash distributions and the potential for capital appreciation, combining income with growth. Both options allow investors to retain control over their assets, unlike annuities, which transfer control to insurance companies.

Ultimately, the choice between annuities and alternatives like IRAs, 401(k)s, or stocks depends on individual financial needs, risk tolerance, and retirement goals. Annuities may suit those prioritizing guaranteed income and longevity protection, but their drawbacks make them less attractive for many. IRAs and 401(k)s offer flexibility, tax advantages, and growth potential, while stocks and bonds provide avenues for higher returns with varying levels of risk. Careful consideration of these factors will help investors make informed decisions about the best tools for their retirement planning.

High-Frequency Sounds: A Painful Noise for Mice?

You may want to see also

Frequently asked questions

Annuities can be a sound investment for retirement planning, especially for those seeking guaranteed income and stability. They provide a steady stream of payments, often for life, which can help manage longevity risk. However, they may not be suitable for everyone, as they often come with fees, limited liquidity, and lower growth potential compared to other investments.

The risks of annuities include inflation eroding the value of fixed payments, high fees and surrender charges, and the financial stability of the issuing insurance company. Additionally, annuities may limit access to your principal, making them less flexible than other investment options.

Annuities typically offer lower returns compared to stocks but may outperform bonds in certain scenarios. They are not designed for high growth but rather for income stability and guarantees. If your goal is capital appreciation, other investments may be more suitable.

Annuities grow tax-deferred, similar to 401(k)s and IRAs, which can be advantageous. However, withdrawals are taxed as ordinary income, and if taken before age 59½, penalties may apply. They may not be as tax-efficient as Roth accounts, where qualified distributions are tax-free.